Foundryecosystem Report: AI, UMC, Tower, Renesas

This report provides a snapshot of the latest announcements in the foundry and other markets

By Mark LaPedus

Foundry vendors are an important part of the semiconductor business. These vendors manufacture chips for other companies in large manufacturing facilities called fabs. Foundries make chips for use in various applications, such as automotive, communications, computing, consumer and industrial.

The foundry business is a dynamic industry. Nearly every week, there are several new and major announcements in the semiconductor foundry market.

To help the industry, Semiecosystem has released the latest edition of its “Foundryecosystem Report.” This report provides a snapshot of the latest announcements in the foundry and other markets. (The report is free for readers.) Here’s what this report covers:

*Datacenter CapEx forecast

*Nvidia’s earnings

*UMC’s management changes

*Tower’s photonic deals

*Renesas’ woes

I have described each item in detail below.

Datacenter CapEx forecast

AI is fueling a large percentage of the growth in the semiconductor industry. So, how long will the AI boom last?

Right now, some believe that the AI market is moving from a boom to a bust cycle. Many in the AI market disagree, saying that the AI industry is still in the early innings of a boom cycle.

In my opinion, the AI market will eventually slow and then hit a wall, perhaps in 2028 or 2029.

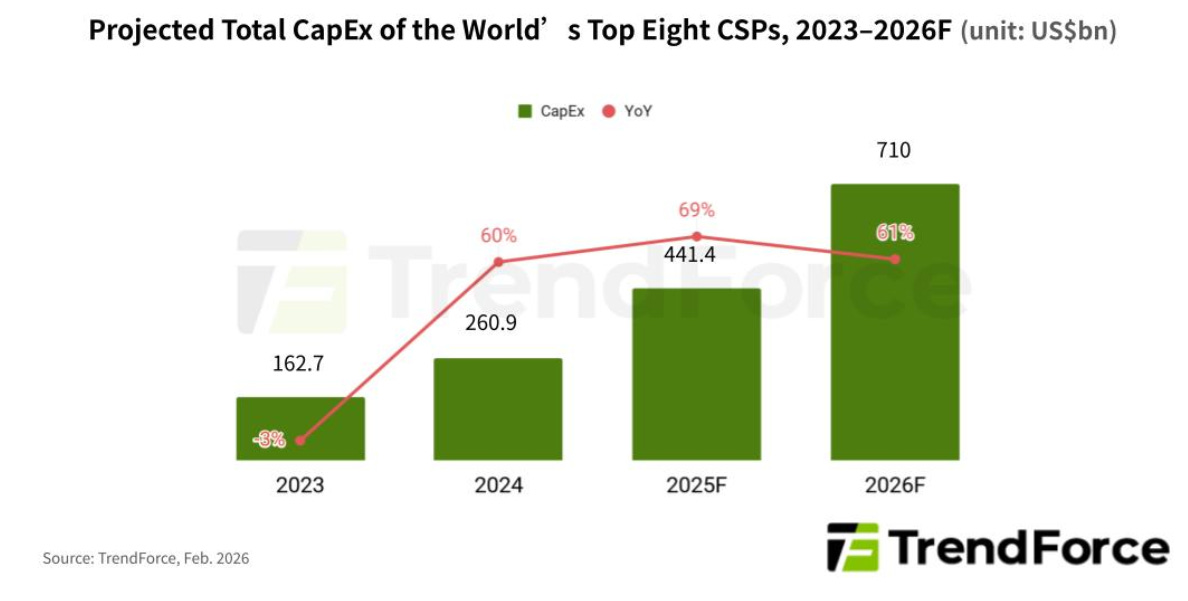

Nonetheless, 2026 looks like a strong year for AI, that is, based on the capital spending plans for leading cloud service providers (CSPs). Combined capital expenditures by the world’s eight leading CSPs—Google, AWS, Meta, Microsoft, Oracle, Tencent, Alibaba, and Baidu—are projected to exceed $710 billion in 2026, representing approximately 61% year-over-year growth, according to TrendForce, a market research firm (See chart below).

These and other CSPs own and operate a number of large computing facilities called datacenters. Datacenters process an enormous amount of data using specialized computers called servers.

There are several types of servers in the market, including traditional and AI-based systems. Traditional servers run general-purpose applications. In contrast, AI servers incorporate more advanced chips like GPUs. These systems handle data-intensive AI workloads, such as ChatGPT algorithms.

The world’s eight leading CSPs—Google, AWS, Meta, Microsoft, Oracle, Tencent, Alibaba, and Baidu—are generally increasing their capital spending plans to meet the booming demand for their respective AI datacenters.

Nvidia’s earnings results

Nvidia, the leader in the AI chip market, isn’t slowing down. The company this week reported record revenue for the fourth quarter ended Jan. 25, 2026, of $68.1 billion, up 20% from the previous quarter and up 73% from a year ago.

Net income was $42.960 billion in the quarter, up 35% from the previous quarter and up 94% from a year ago.

Nvidia’s biggest market is the datacenter. In this segment, the company’s fourth-quarter revenue was a record $62.3 billion, up 22% from the previous quarter and up 75% from a year ago, driven by the major platform shifts — accelerated computing and AI.

For fiscal 2026, revenue was $215.9 billion, up 65% from a year ago. “Computing demand is growing exponentially — the agentic AI inflection point has arrived. Grace Blackwell with NVLink is the king of inference today — delivering an order-of-magnitude lower cost per token — and Vera Rubin will extend that leadership even further,” said Jensen Huang, founder and CEO of Nvidia. “Enterprise adoption of agents is skyrocketing. Our customers are racing to invest in AI compute — the factories powering the AI industrial revolution and their future growth.”

Nvidia’s outlook for the first quarter of fiscal 2027 is as follows: Revenue is expected to be $78.0 billion, plus or minus 2%. It is not assuming any datacenter compute revenue from China in its outlook.

UMC exec changes

Taiwan’s United Microelectronics Corp. (UMC), the world’s fourth largest foundry vendor, has made several major changes within its executive management team.

As part of the changes, Jason Wang, co-president of UMC, will become the new chief executive at the company.

SC Chien, co-president of UMC, will no longer have a management role at the company. Chien has been has elected to serve as chairman of Unimicron Technology, an invested company of the UMC group. Taiwan’s Unimicron is a supplier of printed circuit boards (PCBs), substrates and other products.

Meanwhile, Ming Hsu, executive vice president at UMC, has been named president and chief operating officer at UMC, and has also been appointed a member of the board.

UMC appointed Chien and Wang as co-presidents in 2017, who together led the company’s strategic transformation to focus on specialty process technologies serving high-growth markets. Hsu, who joined UMC in 2003, has been a core member of the company’s senior leadership team.

Stan Hung, chairman of UMC, said: “The leadership changes announced will enable UMC to further strengthen execution and raise decision-making efficiency, while ensuring continuity of our strategic direction.”

Photonic foundry deals

Isreal’s Tower Semiconductor, a foundry vendor, continues to expand its efforts in the silicon photonics market. Tower has recently announced several partnerships in the arena, including:

*Tower and Scintil Photonics announced the availability of a heterogeneously integrated dense wavelength division multiplexing (DWDM) laser sources for AI infrastructure using Scintil’s SHIP (Scintil Heterogeneous Integrated Photonics) technology. SHIP leverages Tower’s silicon photonics platform and combines it with heterogeneous integration of monolithic laser sources, capable of meeting the DWDM technical requirements for AI.

*Tower and Xanadu, a photonic quantum computing company, announced an expansion of their collaboration in developing advanced silicon photonics for fault tolerant quantum computers based on Tower’s silicon photonics platform. These developments build on prior collaborative technical achievements, including a series of joint tapeouts to test and refine Xanadu’s designs on Tower’s process flows.

*Tower and Salience Labs, a supplier of photonic solutions targeting connectivity for AI datacenter infrastructure, announced a partnership to manufacture photonic integrated circuit (PIC) based optical circuit switches (OCS) for AI infrastructure. The collaboration leverages Tower’s silicon photonics platforms, namely, PH18DA with integrated III-V lasers and TPS45PH, with low loss nitride waveguides. The partnership moves from development into pre-production phase, driving product readiness and at-scale deployment for AI datacenter deployment.

Renesas’ woes

2025 was a difficult year for Japan’s Renesas, a supplier of chips for automotive, computing, industrial and other markets.

Renesas’ consolidated revenue for the year ended Dec. 31, 2025, was 1,321.2 billion yen (US$8.8 billion), a 2% decrease over 2024. This was mainly attributable to a decrease in revenue from its automotive chip business. In 2025, the Japanese chip supplier lost 51.8 billion yen (US$330 million).

The loss can be attributed to a disastrous deal with Wolfspeed, a U.S. supplier of silicon carbide (SiC) substrates and devices. In 2023, Renesas entered into a SiC wafer supply agreement with Wolfspeed. Renesas provided a deposit of US$2 billion to Wolfspeed. In addition, the Japanese company was supposed to manufacture SiC-based power semiconductors in 2025.

Back in 2023, the SiC device market was robust. The electric vehicle (EV) market--the big driver for SiC devices--was growing.

Then, the SiC market fell off a cliff. The EV market is still strong in China. But in recent times, the EV market has slowed in other regions. This in turn has caused sluggish growth and overcapacity in the worldwide SiC device market.

On top of that, Wolfspeed last year filed for Chapter 11 of the U.S. Bankruptcy Code. Wolfspeed has since emerged from Chapter 11.

Nonetheless, Renesas has recently halted its plans to make SiC devices. And it recently recorded a large loss on the receivables related to a deposit provided to Wolfspeed.

Meanwhile, in recent times, Renesas has made several moves to regain its footing in the market, including:

*After getting burned in the SiC market, Renesas is now betting on gallium nitride (GaN). Efficient Power Conversion (EPC), a U.S. supplier of GaN power devices, this month announced a licensing agreement with Renesas.

Under the agreement, Renesas will gain access to EPC’s low-voltage GaN device technology and its established supply-chain ecosystem, accelerating the adoption of high-performance GaN solutions across a broad range of markets. EPC and Renesas will collaborate over the next year to establish internal wafer fabrication capabilities for these products. In addition, Renesas will second-source several of EPC’s GaN devices.

*Renesas owns and operates several fabs. These fabs produce chips using more mature processes. In the fourth quarter of 2025, Renesas’ fab utilization rates were somewhere around a mere 50%.

The company needs to better utilize its fab capacity. And it needs access to different technologies. So, it has reached out to the foundry industry for help.

In February, GlobalFoundries (GF) and Renesas expanded their existing foundry alliance. Under this partnership, Renesas will gain access to GF’s technology portfolio, including 22nm FD-SOI, BCD and CMOS technologies with non-volatile memory features to support its SoCs, power devices and MCUs. Tape-outs under this expanded collaboration are on track to begin in mid-2026.

*Then, in a move to cut costs, Renesas recently exited the timing chip business. U.S.-based SiTime has acquired certain assets related to Renesas’ timing business.